LIC is India’s most privileged insurer. So why is it losing its way?

LIC is the unparalleled leader in this massive and fast-growing industry. Formed in 1956 and backed by the government, it currently houses policies with a combined sum-assured of ₹60 trillion, has a share of more than 60% in new business premiums, 70% of individual insurance policies, almost 90% in group insurance policies, and ₹55 trillion in assets under management (AUM). For perspective, the AUM of India’s entire mutual fund industry is ₹67 trillion.

Also read: This stock rallied 500% in four months. Now, its aiming for 6X revenue by 2029.

In 2000, the government opened up the insurance industry to private firms. Competition has increased and the rules of the game have been changing frequently since then. Faced with new regulations that require agility, LIC has ceded market share to private competitors.

As a result, LIC’s clout has been declining. It was listed on the bourses in May 2022 after a record-breaking initial public offering (IPO), but its stock has remained flat even as those of its competitors have rallied.

Influence waning

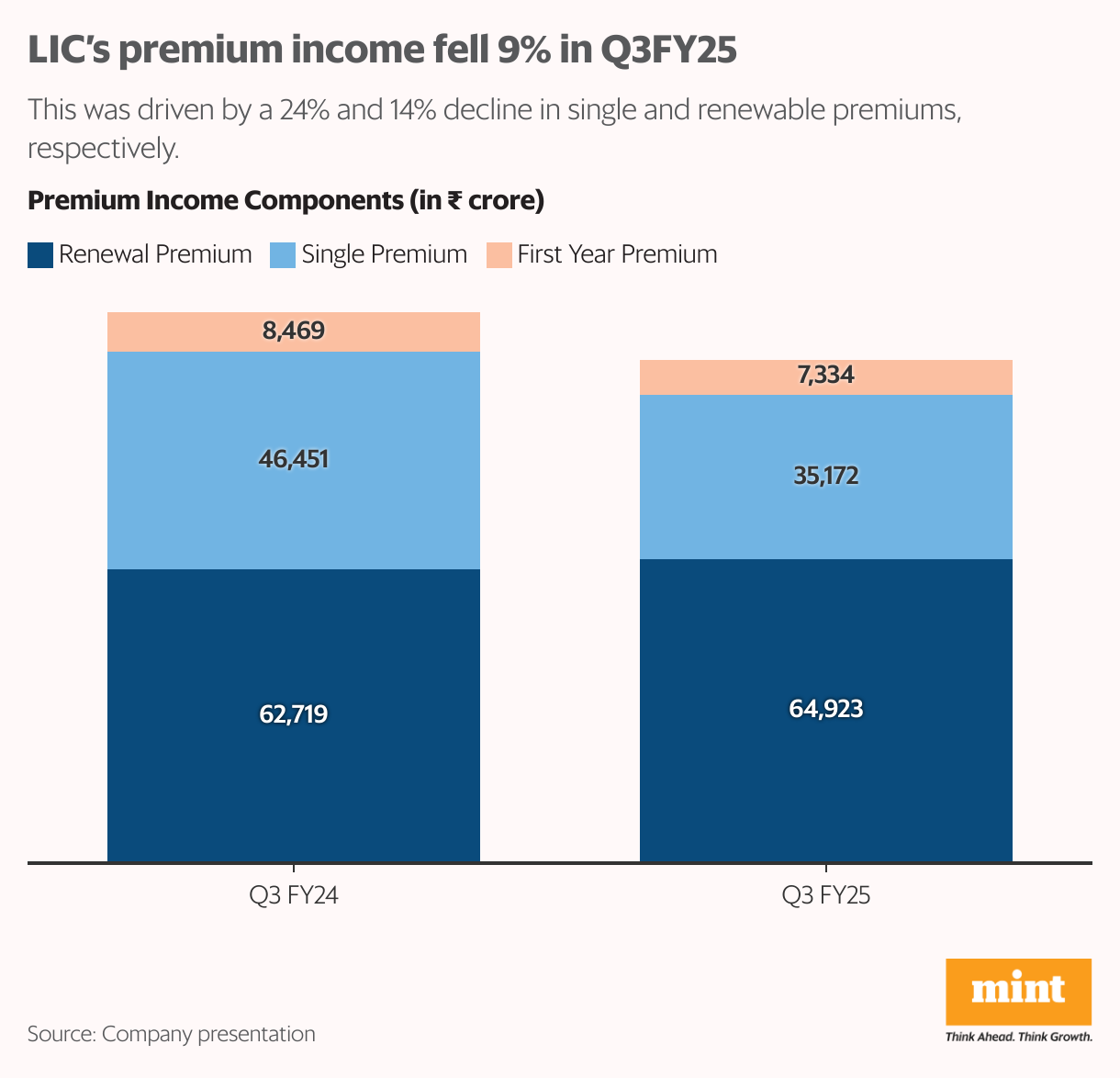

LIC’s influence continued to wane in the December 2024 quarter (Q3FY25), during which net premium income fell 8.7% year-on-year to Rs.1.07 trillion. New business premium declined 21% year-on-year to ₹43,075 crore, while the annualised premium equivalent (APE) dropped 24% year-on-year to ₹9,950 crore (the Street expected ₹10,789 crore). Much of the fall in APE was from individual policies, which declined 27% year-on-year.

The overall expense ratio improved by 231 basis points year-on-year to 12.97% in the nine months to December 2024, led by a 30% drop in employee expenses. This helped increase the bottom line by 17% year-on-year and improve the solvency ratio from 1.93 to 2.02 despite falling premiums and shrinking market share.

In response to these unimpressive Q3 numbers, the stock fell 0.70% on Monday, at par with the Nifty 50 index.

Biggest strengths = biggest weaknesses

LIC’s biggest strengths are its government backing, its humongous size, and its massive offline presence via its agency channel and widespread branches. But it could be argued that these very strengths also double up as its most glaring weaknesses.

Firstly, even as a listed entity, 96.5% of LIC’s shares are owned by the government. While this government backing gives it the implicit trust of policyholders, government ownership has its share of constraints. At least 75% of its investments must be made in government securities, and it is also lends to projects of national interest. This severely limits LIC’s investment avenues. Moreover, profits of government-owned entities are generally more likely to be redistributed than be ploughed back into growing the company.

Also read: MTNL’s 25% stock surge signals relief, not revival

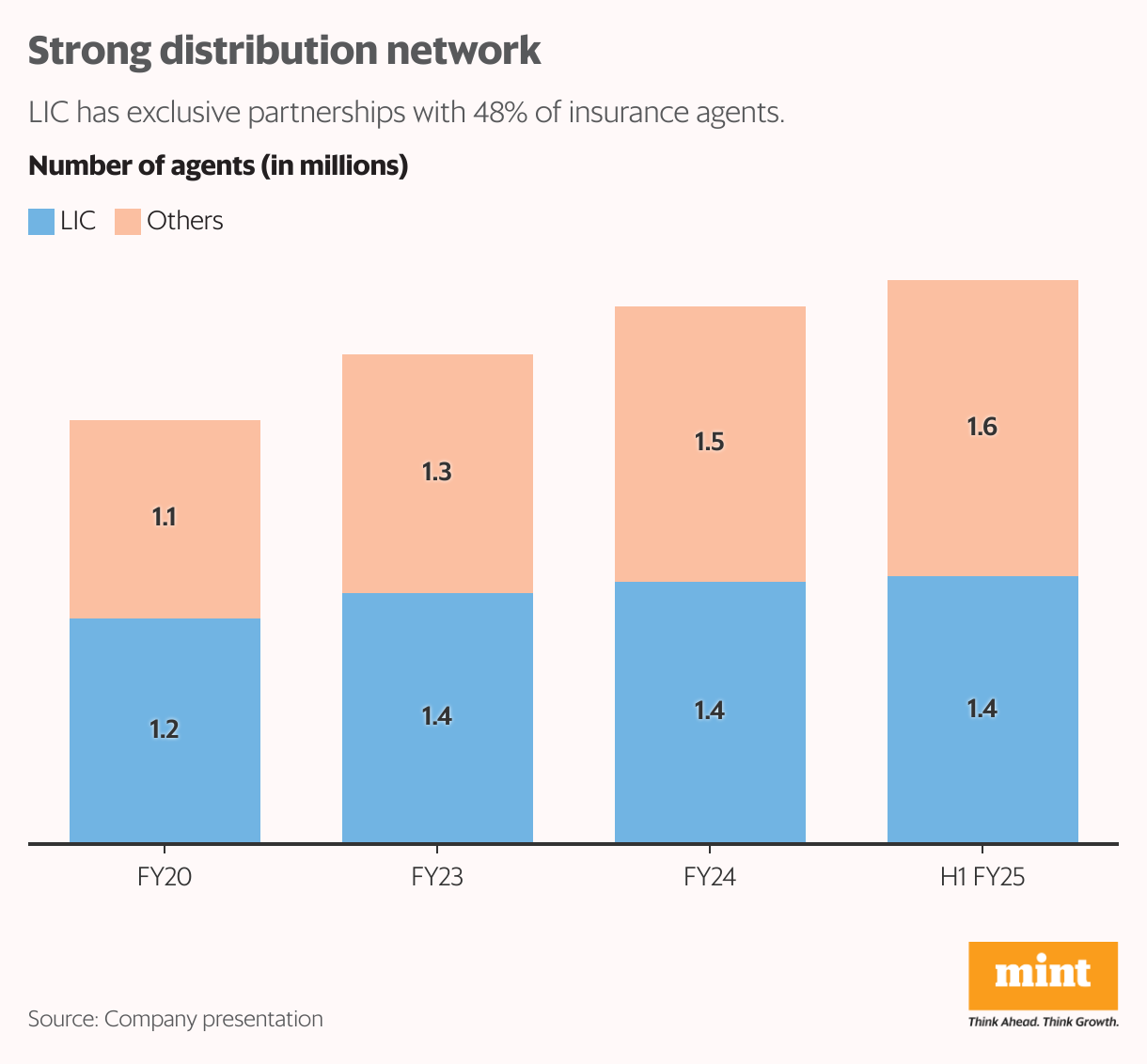

Secondly, LIC has a massive agency distribution network comprising almost 1.5 million exclusive individual agents. It also has around 2000 branches and 1,500 lean satellite offices across the country. For comparison, the largest private insurer, HDFC Life, has less than 500 branches. While this large offline presence lends it credibility and access to the most underinsured segments, it adds significantly to costs at a time when its competitors are moving towards low-cost online distribution channels.

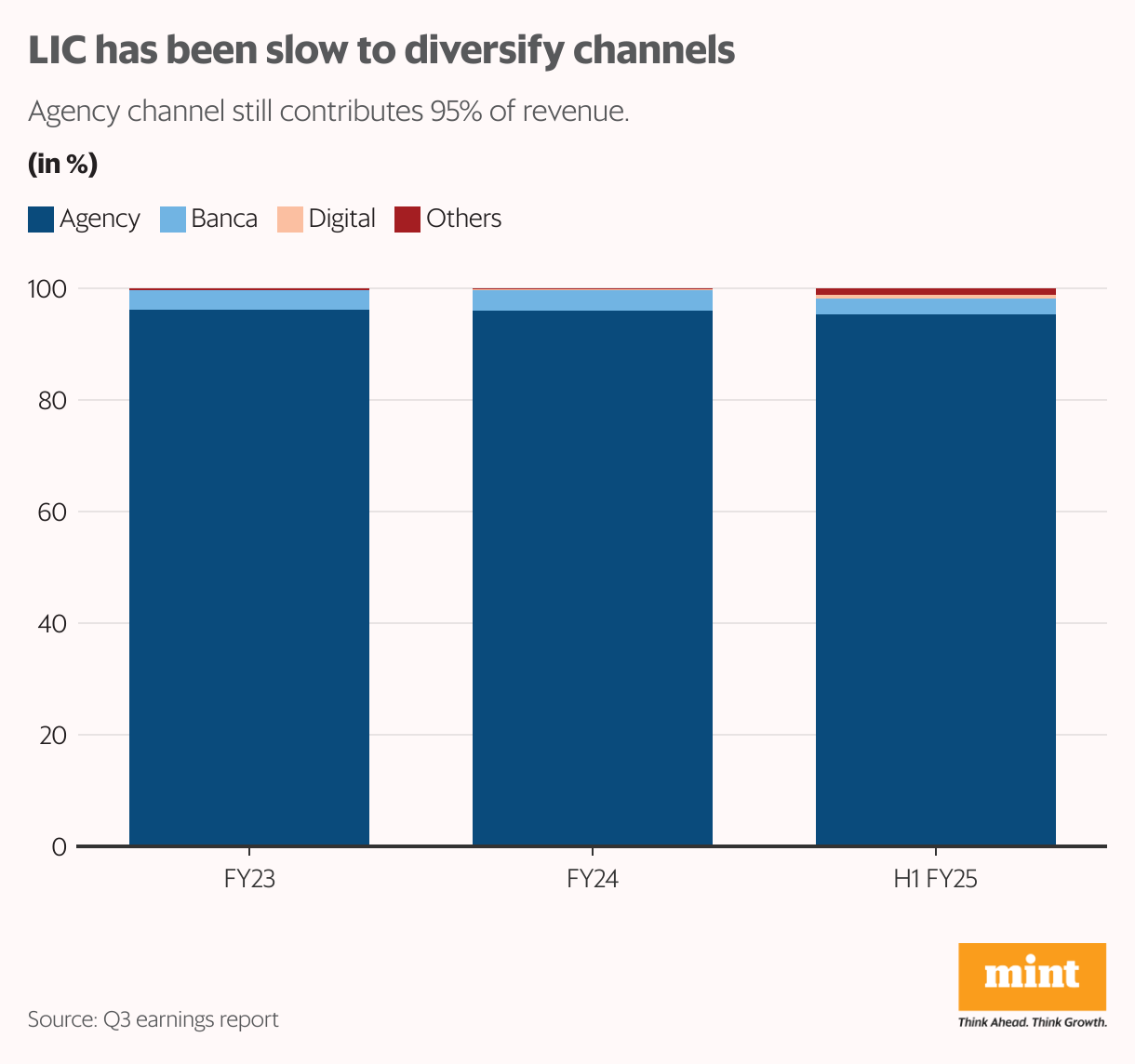

LIC is also excessively dependent on the agency channel, which contributes a whopping 95% of its revenues. More worryingly, the regulatory upheaval around distribution channels (covered in the next section below) puts LIC’s distribution model at risk.

Finally, LIC’s massive AUM gives it huge potential to move the market. At the same time, it makes its profitability particularly vulnerable to volatility in the stock markets.

Regulatory upheaval

The regulatory landscape of India’s insurance industry has been changing quickly, adding to LIC’s worries. From disincentivising insurance policies through tax changes, reducing the surrender penalties, opening up agents to multiple insurers, cracking down on bancassurance, nudging private insurers to get listed, or the latest move to allow 100% FDI in insurance, changing regulations have forced India’s insurers to frequently recalibrate their business models.

While the Insurance Regulatory and Development Authority (IRDAI) introduced measures to ease the compliance burden during the pandemic, regulations introduced since then have made insurers’ lives harder. The incremental incentivisation of the new tax regime, which provides no tax deductions for investments and insurance under Section 80C, has in effect disincentivised investments and insurance. Tax benefits on high-ticket insurance plans have also been removed, limiting revenue growth of insurance providers.

Profitability has not been spared either. Effective October 2024, IRDAI put limits on the surrender penalties insurers charge. While this was done in the interest of policyholders, insurers have had to introduce deferment and clawback provisions on commissions to compensate for the margin impact. LIC has refrained from such cutbacks on commissions in the interest of its agents. Instead, it has increased premiums and minimum ticket sizes (smaller ticket sizes at LIC had seen higher surrenders), while modifying the commission structure – increasing renewal commissions while reducing first-year commissions, and increasing commissions on products with higher persistence.

Also, the Insurance Amendment Act has proposed that agents be allowed to tie up with multiple insurers across life, health, and general insurance (versus one insurer per category). While this would reduce conflicts of interest in the sale of insurance, it would also increase competition in the agency channel, LIC’s bread and butter.

Also read: Bharat Electronics is riding the defence boom. But is it a long-term bet?

Of course, the RBI’s recent crackdown on bancassurance, in which it asked insurers to reduce bancassurance contribution to 50%, has been positive for LIC, given its limited dependence on this channel.

Finally, the Budget proposal for allowing 100% FDI in insurance will intensify competition, with $12 billion of additional foreign funds expected to pour into the industry over time.

What does the future hold for LIC?

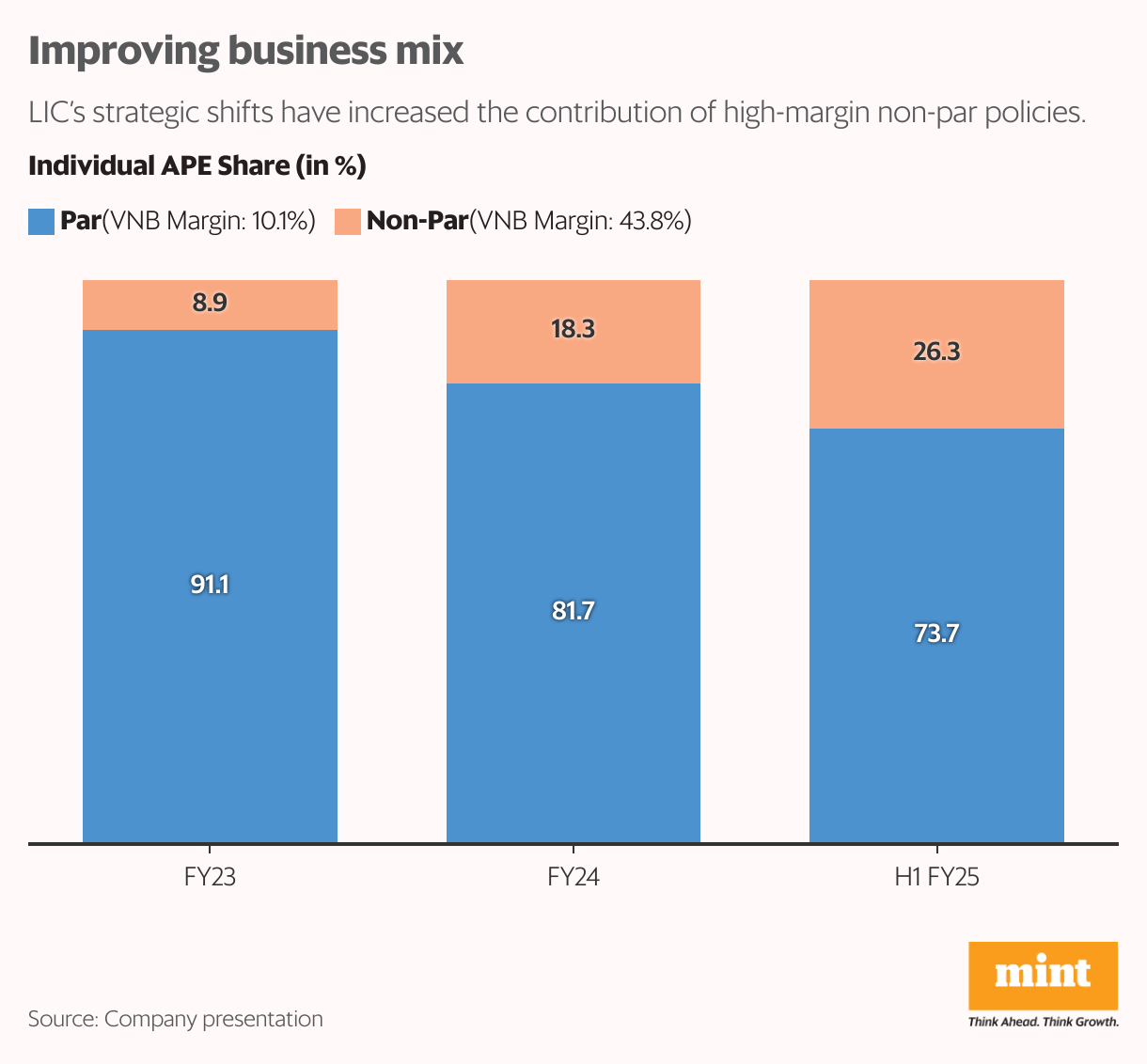

LIC is aware of the cracks appearing in its business model. It is shifting its product mix towards the more profitable segments – protection, non-par and savings annuity – by modifying its commission-structures. Improvements in the business mix have been contributing 4.3% to 4.7% to its overall value of new business (VNB) margins.

It has also increased premiums and minimum ticket sizes while working on improving its online presence and diversifying beyond agent distribution. In fact, 32 of its 54 products have been relaunched so far, with more relaunches expected in the future. It also entered the futures and options (F&O) segment and is also looking to enter the fast-growing health insurance sector.

So far, these proposed changes have led to a sales push for older products before they come into effect, distorting the year-on-year comparison. Some of these changes have caused short-lived spurts in its stock-price, but a sustainable rally will emerge only when its core business of life insurance recovers. While LIC’s strategic shifts are expected to help over the medium to long term, we can only hope that the rules of the game do not change in the time it takes for the benefits to emerge.

For more such analysis, read Profit Pulse.

Ananya Roy (@ananyaroycfa on X) is the founder of Credibull Capital, a Sebi-registered investment adviser.

Views are personal and do not represent the stand of this publication.