EV rush is over, but UNO Minda is positioned better to survive a tariff war

But there have been pockets of strength. For instance, the registration for electric two-wheelers expanded by 37% on-year. The government focus has also continued on new-age vehicles. The budget 2025 announced an exemption of customs duties for components used in electric vehicle (EV) battery manufacturing, and the National Manufacturing Mission has been formed with a focus on clean tech manufacturing to improve the EV charging ecosystem.

Against this backdrop, the Gurugram-based auto components manufacturer UNO Minda caught investors’ attention around the middle of 2024 when it entered into a technical license agreement with Inovance Automotive (HK) Investment. This development sparked hopes of Minda expanding its EV footprint by leveraging Inovance’s expertise in EV powertrain technology. Investors rejoiced, sending the stock skyrocketing by 60% in less than three months.

But this EV rush didn’t last long, and UNO Minda has corrected by almost 30% since then. This month, there has been an uptick due to its limited international exposure in an increasingly protectionist world order. But will this optimism persist?

Reason the EV rush didn’t last longer

Minda’s EV revenues have been growing exponentially. In the December quarter, EV sales for Minda grew by 45% on-year. While these sales have been driven by the sales of low-voltage EV components to two-wheeler original equipment manufacturers (OEMs), Minda has also started winning orders from four-wheeler OEMs for components, including battery disconnecting units and EVSE-wall mount charging units.

It is also engaged in the self-development of other four-wheeler EV components, such as acoustic vehicle alert systems, high-voltage integrated charging units, and electric drive units.

UNO Minda also extended its collaboration with Inovance into a 30-70 (Inovance-Minda) joint venture in February to develop high-voltage EV powertrain components for PVs and CVs. Minda’s capacity expansion plans, spanning five to six years for EV-specific components, are expected to further help its EV business.

That said, it is important to note that EV is still a small part of Minda’s business. In the latest quarter, EV contributed ₹238 crore to Minda’s revenues. That is less than 6% of its total revenues. In fact, more than 95% of its product portfolios are powertrain agnostic, which indicates that the focus on EVs is still in its nascent stage. So, it will be a while before the EV initiatives start bearing tangible fruit.

Low global exposure has been a blessing

UNO Minda’s subsidiary in Europe, Clarton Horn, has been facing headwinds from rising costs of production, cheaper imports, and a slow transition to EVs. However, since only 11% of UNO Minda’s revenues come from international markets, including Europe, the impact of Europe’s challenges on overall revenues has been limited. Going forward, expansion in Indonesia is expected to diversify international exposure beyond Europe.

Furthermore, as the US imposes tariffs on auto imports, the direct impact on UNO Minda is expected to be low, given its low international exposure. As Trump’s tariff threats intensified this month, UNO Minda shares have appreciated by more than 9%, while the broader Nifty Auto Index has remained flat.

However, given that OEMs serviced by UNO Minda have significant international exposure, the indirect impact of tariffs on UNO Minda cannot be ruled out.

Mainstay products have slowed down growth

While the broader auto industry has grown by 7% on-year, UNO Minda has significantly outperformed with 18.8% growth in revenues during the period. But it is important to note that while the company’s mainstay products include switching and lighting systems, castings, seatings, and acoustics, the latest quarter’s revenue growth has been driven by 46.2% growth in “other products”. This can be attributed to new product launches and growth in EV component sales.

Meanwhile, despite a recovery in the two-wheeler market, premiumization, and capacity expansion, its primary products—switching systems, lighting systems, and castings—which contributed two-thirds of its revenues, witnessed relatively mellow growth in the range of 12% to 15.3%.

At the same time, challenges in Europe’s agricultural vehicle sector have led to degrowth of 0.4% in the seatings segment despite the commencement of pneumatic seat manufacturing for domestic CVs. Its European subsidiary, Carlton Horn’s challenges are reflected in the 9% degrowth of acoustics revenues.

Segment positioning has worked in its favour

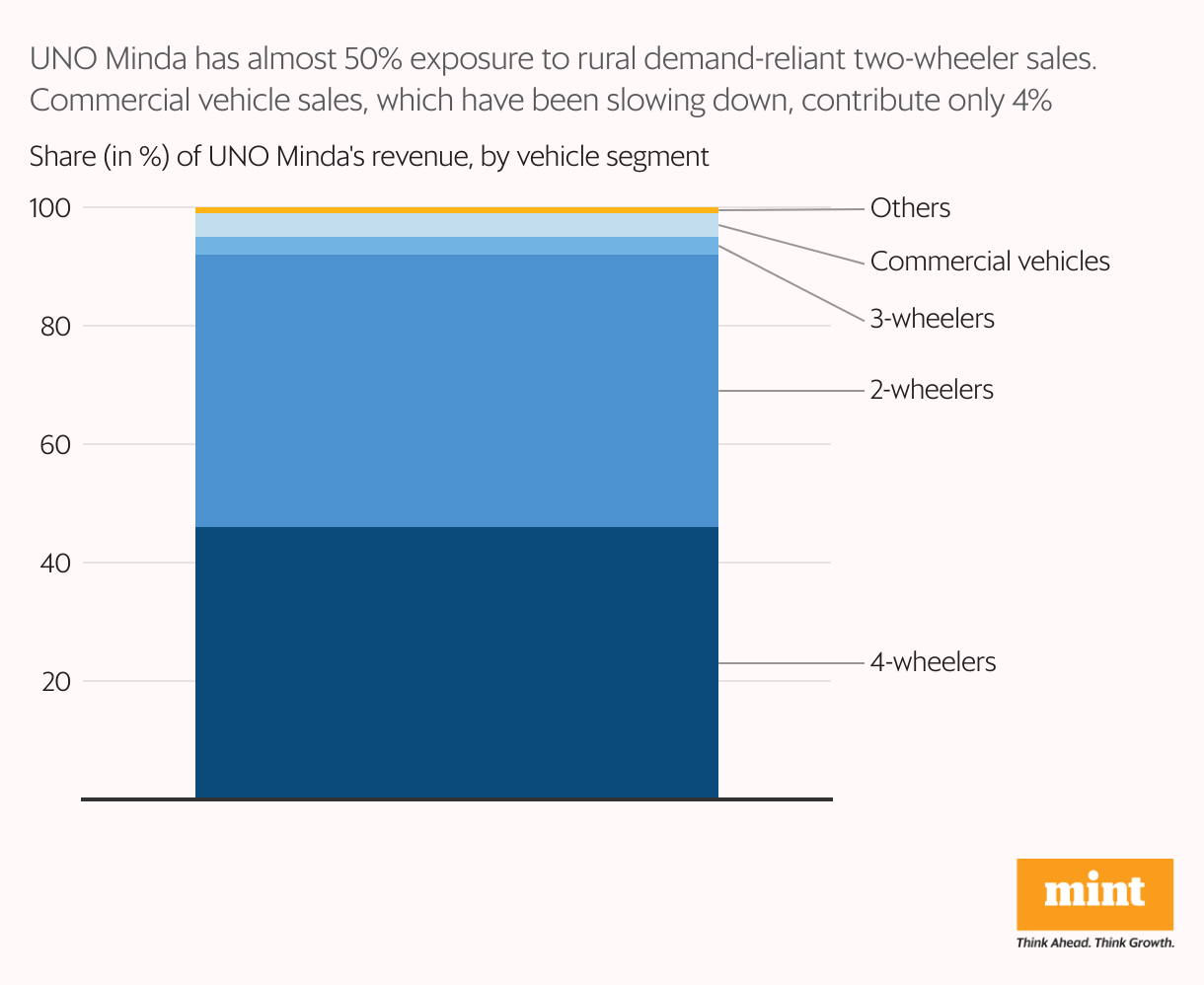

With healthy monsoons and government support, domestic rural demand has recovered. This has led to 8% on-year growth in two-wheeler sales, even as the overall PV segment grew by a meagre 3%. UNO Minda has benefited from this trend, as almost half of its revenues are derived from sales to two-wheeler OEMs.

On the other end of the spectrum, we have CV sales, which have shrunk by 2% on-year. As the government prioritizes fiscal deficit, government capex has slowed down. FY25 government capex is expected to close at a little over ₹10 trillion, falling significantly short of the targeted ₹11.11 trillion.

To make matters worse, in an environment marked by persistent geopolitical and economic uncertainty, private capex has been waiting on the fence. This has resulted in low infrastructure spending. Combined with high vehicle costs due to the transition to BS-VI emission norms, domestic CV sales have been impacted. UNO Minda has remained relatively insulated from this slowdown, as only 4% of its revenues come from sales to CV OEMs.

Capacity expansion to fuel growth

UNO Minda has undertaken capacity expansion worth ₹2,790 crore in projects spanning five to six years. This includes the new greenfield plant for switches at Farrukhnagar and a four-wheeler lighting plant at Pune, which have already commenced operations. Two-wheeler alloy wheel manufacturing capacity has been increased by 50% to 6 MPA. The merger with Kosei, which recently received approval from the National Company Law Tribunal, can also be expected to further revenue growth.

That said, capacity expansion will continue to weigh on the company’s net debt, which increased to ₹1,964 crore in December 2024. Still, thanks to the accumulation of reserves over the years, the debt-to-equity ratio has improved to 0.25x in 2023-24 from 0.4x in 2019-20.

Margins can pick up over the long term

Rising costs of raw materials led to 46 basis point compression in gross margin in the latest reported quarter. Furthermore, interest costs spiked up to ₹47 crore in Q3FY25, up from ₹29 crore in the year-ago period. However, thanks to the company’s lean manufacturing and automation initiatives, Ebitda and PAT grew faster than revenues at 20+% year-on-year. Ebitda is short for earnings before interest, taxes, depreciation and amortization.

For more such analyses, read Profit Pulse.

Going forward, over the medium term, interest expenses can be expected to pick up further and weigh on margins. But as capacity utilization improves, extending the trend of rising margins seen over the last few years, operational leverage can be expected to help support margins over the long term.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold any shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.